![]()

Following a recent Tribunal decision, the leading North-West law firm Brabners faces a £68,000 VAT bill for electronic local authority property searches it obtained by using a search agency, after the tribunal ruled that they should not have been treated as disbursements for VAT purposes, notwithstanding that Brabners was supported by the Law Society in presenting its case.

The Law Society has stated it is considering the implications of this decision for its practice note on VAT and Disbursements, however it is not yet known whether there will be an appeal to the Upper Tribunal. Strictly speaking, First Tier Tribunal decisions have no bearing in law, and do not generally set legal precedent.

The ILFM’s recommendation is to protect your position by treating these types of transactions in accordance with HMRC’s view, which is that the VAT liability of the recharge to the client will follow the VAT liability of your overall supply to the client, and thus almost inevitably will be subject to standard rate VAT. This will only impact on transactions where VAT has not already been charged on the original cost. There should not be any cost to the practice, as it is the client that will suffer the additional VAT.

As stated above, there could be an appeal, and so firms may choose to delay changing their current practice as the decision could yet be overturned, but clearly there is a risk to taking this course of action if the decision is upheld. We would recommend involving your COFA in the decision as to how your firm treats such searches. You should also review whether any change is needed to your quotes and your terms of business to allow for VAT being added.

ILFM Executive Council

27th September 2017

Here is some extra information from recent Questions and our Answers

Q. For searches where the supplier does not charge us VAT, I understand that we will need to show the search in the fees section of the bill to the client and add vat. But for searches where the supplier does already charge us VAT, do we also need to show that disbursement under the fees section? Perhaps as although the cost/charge is the same we are providing a service?

A. In both cases you should show the recharge of the search fee under profit costs, not disbursements. VAT will need to be added to the net of VAT amount.

Q. Does this only apply to local authority property searches that we carry out on behalf of our client, or does it also apply to local land charges, coal mining searches, draininage etc? Obviously this would also depend on your answer to Q1.

A. The Judge in the Tribunal was only looking at electronic property searches. However, as his logic in this case could arguably be applied to other types of search, the ILFM’s recommendation is that firms consider adding VAT on all searches from now on. Where search providers already charge firms VAT on the supply, there should be no additional cost to the end client. However, where searches have historically not carried VAT, clients will in future have small additional amounts of VAT to pay.

Q. Does this only apply to electronic searches, and not to searches requested via letter / cheque? Although the guidence refers to electronic searches, surely the outcome and service provided is the same?

A. See comment above.

Q. If the search is requested for client 1, but then not required and charged to client 2, presumably this is treated in the same way as if client 2 had purchased the search in the first instance?

A. Yes.

Q.

I refer to the recent information received concerning VAT and electronic local authority searches.

At the moment we use the agency method when charging out. We do not claim VAT and we do not pay VAT.

If the search fee is £100 + VAT £20 = £120 how would it appear in the bill of costs and what section would it be under - disbursements paid?

A.

Treat as a VAT-able disbursement in the books by reclaiming the input VAT and then recharging the net value and same amount of VAT to the client. This will result in VAT neutral so no net cost to you or the client. Make sure it’s not shown in the disbursement section of your VAT invoice and it itemised as an addition charge in the charges section of the VAT invoice.

Q.

We have just received the info from ILFM on the Brabners disbursement case. It is a little confusing but I assume that they hadn’t charged out full VAT on searches, even though there was not VAT on some of the local search.

Looking at one of our invoices, the local search has disb £41.55, search fee £69.54, net search fee £111.09, VAT £13.91, total fee £125. I assume this should be charged out at £111.09 plus £22.21 vat, total £133.30, meaning a total extra cost to the client of £8.30.

The ILFM note suggests amending quotes to clients so I assume this is right, but would be grateful if you could clarify.

A.

Your assumption is absolutely correct. The additional VAT will be a cost to the client.

Q.

Please can you advise on how we should bill our clients for non-vatable searches should we add on vat ?

A.

Due to the complexity of these types of disbursements, can you give me an example of what is considered to be a non-VATable disbursement.

Q.

I mean in light of the new ruling on electronic searches from search agencies.

How should I treat these when the payment is charged from our office account and we then include this on our bill to the client.

Advice I have had so far is we need to be adding vat on but this would mean an amount of vat would be charged to our office account and wouldn’t be picked up when reconciling our accounts.

How are you advising members to treat electronic searches that have no vat

A.

You would need to treat the search agency supply as having been to your business as an overhead (which it is) and then recharged by you as an additional charge when billing.

Where the search agency charge is net and VAT at 20%, this is straight forward as you would post as a VATable disbursement, reclaiming the VAT. When billed, you would bill the same net and VAT value resulting in VAT neutral. No net cost to you or the client.

However, where the search agency service has no VAT or an element of the search is non-VATable, you need to process through accounts exactly as is on the supplier invoice and then when billed, you charge VAT on top of the net value. The additional output VAT will be a cost to the client.

Make sure in both instances, the search fee is not itemised as a disbursement on the face of your VAT invoice. It should be itemised in the charges section of your invoice.

Q.

Please advise on the application of the VAT ruling in respect of the Search Fees via electronic providers.

Currently an invoice is issued by the supplier including some items include VAT and others which are zero rated. The entire gross amount is posted as a disbursement to the client ledger and included on the Cash Statement to the client.

Does the VAT ruling mean that the gross figure from the supplier should be include in a bill and 20% VAT applied even though VAT has already been included on some items, or that the VAT needs to be added to the items that are currently zero rated? Alternatively, should the invoice be posted to a nominal where the VAT is claimed as the firm's expense and the net figure journalled to the ledger for the disbursement to be billed and VAT applied at this point?

I would be very grateful for your guidance as I am a remote cashier looking after 3 firms with this query. Thank you for your help.

A.

"Alternatively, should the invoice be posted to a nominal where the VAT is claimed as the firm's expense and the net figure journalled to the ledger for the disbursement to be billed and VAT applied at this point?”

Absolutely. Treat as an office overhead and then recharge the net value of the search fee plus 20% output VAT.

Q.

At the moment we are charged vat on local searches by the search agency on the original cost - and the gross figure is treated as a disbursement for vat purposes and the client pays the gross figure. This transaction goes through on client account and does not go through the firms vat account. So am I right in assuming this will stay the same?

HMLR searches & registrations do not show vat and we do these ourselves so I assume they will come under the new ruling (if the appeal is unsuccessful) .

Look forward to clarification from a member of your team.

A.

Firstly, the Tribunal case was specifically in relation to electronic searches obtained through a Search Agency provider.

Where the Search Provider invoices you net and VAT, you need to process this cost to the business as an overhead and then recharge as an additional charge to your client. For example:

A £100 invoice with VAT of £200 input VAT would need to be processed as a net, reclaiming the £200 as input VAT. If you’re Accounting system does not have the ability to record Expenses/Recharges through the Client’s ledger, Office side, you will need to process as a VAT-able disbursement through the client’s ledger, Office side.

When you bill this to your client, you will need to bill the net value plus output VAT of 20% to the client. This will result in VAT Neutral and no net cost to your business or the client. Please note, the Search Agency fee MUST be itemised as an additional charge on your invoice and not a disbursement.

However, where the search agency service has no VAT or an element of the search is non-VATable, you need to process through accounts exactly as is on the supplier invoice, and then when billed, you charge VAT on top of the net value. The additional output VAT will be a cost to the client. Again, itemise as an additional charge on your invoice. SEE BELOW invoice example of recharged overheads to clients.

In terms of LR Searches - if you have commented/advised on the search in detail, then VAT is applicable as you have added value. If you have only had a cursory look - paid on as non-VATable disbursement.

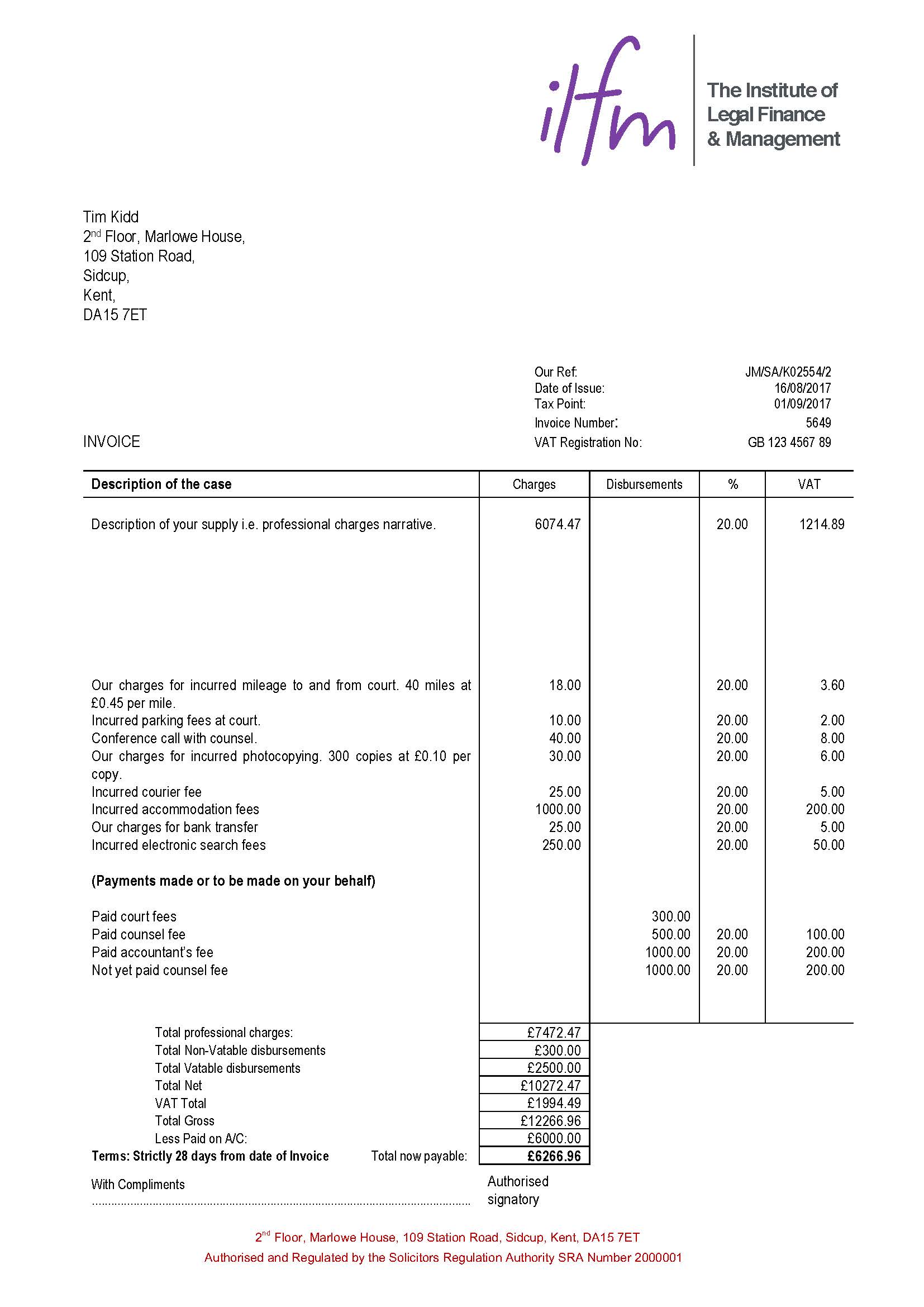

Example....

We use a search agency. If this charge goes on the client's completion statement, not the invoice, would this need to be changed or can we continue to do this?

Dear Jenny,

Thank you for your enquiry.

If you use a Search Agency like Property Search Group or TM for example and you pass on the Search to the client without comment or advice, then you may be able to pass on the cost of the disbursement as Disbursement for VAT Purposes and only show on your completion statement. However, any charge made by the search agency in obtaining the searches on you behalf would be to your firm and not the client. This element of the suppliers invoice must be treated as a recharged overhead when invoiced back to the client. Don’t forget, each payment and the circumstances in which it was incurred when providing services to the client must be first ascertained before you decide whether a payment qualifies to be a Disbursement for VAT Purposes or what HMRC refer to as, a ‘Recharge' (recharged overhead) The reason for this is because some can be either depending on who received and used the third party service/supply.

HMRC’s stance is that 99.9% of the time, a solicitor uses and advises on the contents of the search (not including statutory charges like land registry searches). This then results in the search fee becoming a cost component of the business i.e. a recharged overhead and forms part of your overall service/supply to the client. If your overall supply to the client is subjected to standard rated VAT, then the same VAT rate must be applied to any additional recharged overheads included on your invoice as they’re additional charges outside of fees.

IF - and here it’s a big IF, you can prove you did not advise or comment on the search results and simply passed the document on to the client to make an informed decision themselves, then, and only then may you pass it on as a Disbursement for VAT purposes i.e. not accounting for VAT and not including it on your VAT invoice to the client.

Everything covered within this forum is predicted and applies to UK Vatable entities. What do you do if you have a client whom is not subject to UK VAT, and therefore normal course would be to No VAT or Outside of Scope rate a foreign entity?

The point being that the expectation of the client being domiciled either outside or within EU that VAT would not be payable on services (costs) or disbursements. How do you deal with recovering VAT then, or is it permissible for you to reclaim input VAT with HMRC on UK Property or Land Registry searches, and not charge Output VAT? This in principle would be in breach of VAT compliance but how exactly are we supposed to cope. My firms client base are almost exclusively non-UK and offshore based.

We collect the gross amount from clients on account of searches and then the gross amount is paid from client account. There is no input/output tax as the funds are dealt with from client account and I can see that VAT is shown on the invoices from our search provider. On the completion statement for clients, the searches are listed as the gross amount including the VAT. We use a search provider for some parts but go direct to the Local Authority for our Local Searches. Part of the Local Search - the LLC1 does not attract VAT and therefore we would not claim VAT on that part from the client. As we have been going direct to the Local Authorities, does this affect us? Should we make changes to the above pending the outcome of the appeal?

Thank you for the advice.

With searches being done at the beginning of a file, and the average life span of a sale/purchase being 3 months, depending on how many completions you do, you could be looking at a large increase in debtors / drop in cashflow unless you invoice for searches separately sooner.

The case seems to refer to searches obtained by a search agency. Do these include Land Reg searches? We obtain our own, are they to be treated the same way?

What if the case is succesfully appealed and we have charged vat to client's on searches that we were not charged vat on. Will we have to refund clients?

We have a variety of search providers some make no exempt rated charges, Searchflow (the provider in the Brabners case) makes a flat fee exempt charge on every invoice, some make a different exempt charge depending on the local authority - these range widely. I would love to know why there is such a disparity.

Some invoices include an indemnity policy and I assume we do not need to charge the client VAT on that element

Some fee earners pay the searches out of Client account and so no Input or Output Vat, others come out of Office as the provider insists on payment by Direct Debit. We take money in advance to cover searches. We transfer regularly from Client to Office to improve cashflow. Our system picks up the vat element correctly i.e. the Input VAT we have suffered is recovered and also appears as Output Vat.

Following the case all our search payments will be made from Office and VAT will be charged to the clients on all even the exempt element. I am fairly confident we have got this right. My problem is that the accounts software we use (Videss) will not pick up Output Vat on the exempt element until such time as that is actually billed. therefore we can't make a Client Office transfer against that part of the search. Not a big cash flow problem as that element is fairly small.

It is my understanding that we should be making transfers from Client to Office as the Client money becomes Office money when the disbursement is paid. This means we can't comply with both SAR and HMRC on exempt search charges. Anyone else having the same issue?

This Q&A has been really helpful, but as far as I can see, there wasn't an 'invoice example of recharged overheads to clients' attached to the answer. This would be really useful and I'd be grateful if it could be attached.

Thanks very much

9th October 2017 11:05 "Thank you for your comment. We have added as requested." ILFM