Could you be breaching the Accounts Rules with your suspense ledgers (often known as "suspense account")?

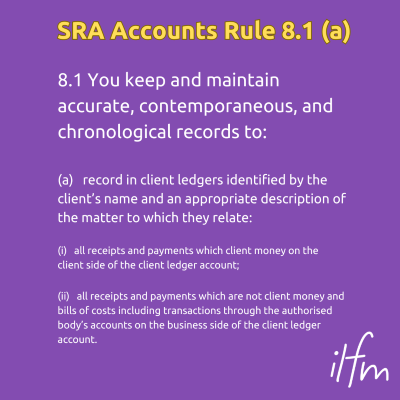

For those that aren’t aware, the main regulator, Solicitors Regulation Authority (SRA), has a specific rule to adhere to in their Accounts Rules 8.1.(a) when it comes to keeping client ledger records.

What is a suspense ledger?

A suspense ledger is used to temporarily record items that are unidentified or cannot be recorded to the accounts yet. In a UK law firm, a suspense ledger must only be used as a short-term “holding” account and any funds placed in it should be investigated and dealt with, no later than 30 days.

If you don’t want your law firm to breach the rules by accidental misuse of a suspense ledger it is best to keep accounts staff, and others (and the whole firm’s reputation) protected by continued professional development training with the ILFM.

The SRA’s guidance has all the information you would need for “Planning for and Completing an Accountant’s Report”; when a suspense account can be used, and how they are indicative:

- Above adequate

- Adequate

- Below adequate

Below is the SRA terminology in better text.

SRA Guide - Above Adequate

Where suspense accounts are used, items are usually no more than, for example, five days old.

SRA Guide - Adequate

Where a suspense account is used, items are usually no more than, for example, 30 working days old.

SRA Guide - Below Adequate

Widespread unjustified use of suspense accounts.

No process for clearing suspense accounts or outstanding items not followed up.

Examples of misuse of suspense ledgers

The following are some classic examples of suspense ledger misuse:

- Using suspense ledgers to hold client money for longer than necessary, instead of returning it promptly to the client or transferring it to the correct account.

- Using suspense ledgers to hide errors, discrepancies, or misappropriations of client money.

- Using suspense ledgers as a substitute for proper accounting records or systems.

- Using suspense ledgers for personal or business transactions that are unrelated to client matters.

Improper use of suspense accounts can result in possible:

- qualified accountant's reports,

- disciplinary actions, and

- criminal charges for fraud or theft.

Does your practice have clear policies and procedures for managing suspense ledgers? Are they regularly reviewed and cleared?

Suspense ledger problems – questions to ask yourselves

Ask yourselves or your colleagues about why there might be an overuse of suspense ledgers.

- Why does the firm receive so many deposits that it cannot immediately identify?

- Are there matters still open?

- Is there a breakdown in communication between fee earning and accounts staff?

- Do the above questions point to wider system weaknesses and wider risks?

Using the suspense ledger to record receipts and payments for matters that might be thought of as too small to warrant opening a separate matter file/ledger? This is a clear breach of the SRA Accounts Rule 8.1(a).

Solicitors Disciplinary Tribunal (SDT) cases where Suspense Ledgers were involved

The Solicitors Disciplinary Tribunal (SDT) is an independent body that hears and decides cases of alleged misconduct by solicitors and other regulated individuals in the UK. The SDT has the power to impose sanctions such as fines, suspensions, or strike-offs from the roll of solicitors.

The SDT lists cases where solicitors have misused suspense ledgers to conceal errors, avoid detection, or manipulate their accounts.

To give you clear examples of SDT cases where there has been a misuse of suspense ledgers, we have listed a few below.

Suspense Account Examples of Misuse

March 2021

SRA v Gary James Burns

The SDT ordered that Gary James Burns should be struck off the roll for making untrue statements to mortgage lenders and clients, failing to complete post-completion formalities, and using a suspense account otherwise in accordance with rule 29.25 of the Accounts Rules, and in breach of principles 2, 4, 5 and 6 of the SRA Principles 2011.

The SDT said that Mr Burns had set out, in some considerable detail, his views about the shortcomings and lack of competence of the administrative and secretarial support he received. The tribunal did not consider it to be credible that, given such strongly held convictions, he would rely to such an extent on the same individual for tasks of such importance.

Legal Futures Headline Conveyancer blamed secretary to “cover up lack of progress”

Mr Burns had acted dishonestly in all respects.

December 2020

SRA v Karamjeet Kaur & Yasar Malik

The SDT ordered that Karamjeet Kaur and Yasar Malik should be struck off the roll for various breaches of the SRA Accounts Rules 2011, including using suspense ledger accounts to hold client money for longer than necessary, transferring client money to office account without proper justification, and failing to keep proper accounting records.

Legal Futures Headline Solicitor’s mismanagement combined with the COFA’s incompetence

They had both acted dishonestly in respect of some of the allegations.

February 2019

SRA v Michelle Hind

The SDT ordered that Michelle Hind should be struck off the roll for dishonestly misappropriating client money, falsifying bank statements, and using suspense ledger accounts to conceal her misconduct.

Legal Futures Headline Solicitor put “financial gain for family” before clients

Hinds had also failed to cooperate with the SRA investigation and breached several SRA principles and outcomes.

AND finally…. there has been a recent SRA decision on a firm of solicitors, Ross Coates Solicitors, that was subject to successive Qualified Accountant’s Reports. These reports raised that the law firm had operated a suspense ledger for unallocated client money. The SRA subsequently conducted an onsite inspection of the firm to review its books of account. Have a specific look at b. below:

The Facts of the Case

Between 2019 and 2022 Ross Coates Solicitors (the “Firm”) had been subject to successive Qualified Accountant’s Reports. These all raised that the Firm operated a suspense ledger for unallocated client money.

Following the SRA’s onsite inspection, it was noted that:

The Firm’s historic client balances’ position had increased since a previous inspection conducted by the SRA identified the same issue.

The Firm operated a suspense ledger that allocated funds it could not allocate to specific clients.

At the time of the closure of our previous investigation (June 2020), the Firm had reduced its residual balance position from 714 balances totalling £32,405.99 to 22 balances totalling £3,477.22. The Firm was issued with a Letter of Advice on 30 January 2020 noting that there had been a large number of small balances on the ledgers for a number of years and that a miscellaneous ledger was used to record unclaimed client ledger balances.

This rose to 360 matters totalling £40,176.05 to the period ending 31 December 2021, where a client balance was held but there had been no ledger movement for six months or more. Enquiries with the firm identified that there was no policy in place to deal with residual balances.

The Firm also operated a suspense ledger from May 2007. Up until 31 March 2022, 778 transactions were posted to it with a balance of £32,334.35. The Firm's accountant’s reports for the periods 2019-20, 2020-21 and 2021-22 were all qualified identifying this ledger as a breach of Account’s Rules.

You can read the who SRA case here: https://www.sra.org.uk/consumers/solicitor-check/184736/

Correct Account

A suspense account is an account or ledger used to temporarily store transactions for which there is uncertainty about where they should be recorded. Once the legal cashiers and accounting staff investigate and clarify the purpose of this type of transaction, it shifts the transaction out of the suspense account and into the correct account. An entry into a suspense account may be a debit or a credit. It is useful to have a suspense account of course, rather than not recording transactions at all until there is sufficient information available to create an entry to the right ledger. Otherwise, larger unreported transactions may not be accounted for.

Suspense Accounts Summary

Are you aware that there are several accounts set up as “suspense ledgers” in your business? Whether you call them “miscellaneous”, or they are under a fee earner or partner’s name, make sure you know that those accounts should only be used for temporary items (such as an unidentified receipt). Do you feel you have the confidence to stand up to a partner or fee earner and ask for clarification of which client matter that receipt should be on?

The SRA is cracking down on suspense accounts, and from reading just some of the above cases, it will help your case in feeling confident to speed the balances on those miscellaneous ledgers to the proper accounts. In a law firm we all play our part in being responsible for entries, missing information, looking at certain transactions, researching and checking on unidentified transactions at least on a quarterly basis.

To summarise, make sure you allocate those “temporary” funds and make sure you do it accurately. Make sure you transfer them away from the suspense ledger BEFORE 30 days at the very latest. Feel confident for further investigation or further analysis on the use a suspense account. Work with your legal cashiers and fee earners alike to move swiftly away from liability suspense account problems.

Being proactive is best practice, by consistently reviewing any suspense accounts. If you are a COFA or in Legal Finance and not a member of the Institute of Legal Finance & Management, then please consider gaining membership HERE for on-going support and training. You can contact the ILFM for further information at any time.

Comments